Oil markets spent Monday frozen, waiting to find out whether the Strait of Hormuz reopens or the war deepens.

Iran rejected the latest ceasefire framework on Monday, hours before Trump's 8 p.m. ET Tuesday deadline. The proposal, a 45-day halt to hostilities brokered by Pakistani military officials and backed by Qatari and Swiss intermediaries, would have required Iran to reopen the strait to commercial traffic immediately. Tehran pushed back, calling the timeline unrealistic and the terms unilateral.

Trump responded by expanding his threat list. The U.S. would destroy "every power plant, every bridge" in Iran if the deadline passed without a deal.

A Market Priced for Maximum Uncertainty

WTI crude is trading around $112 per barrel, Brent around $109. Both have been swinging $5 to $6 intraday as headlines break. The WTI premium to Brent, an inversion that has never persisted this long in modern oil market history, reflects U.S. pipeline crude moving freely while seaborne barrels remain bottlenecked at Hormuz.

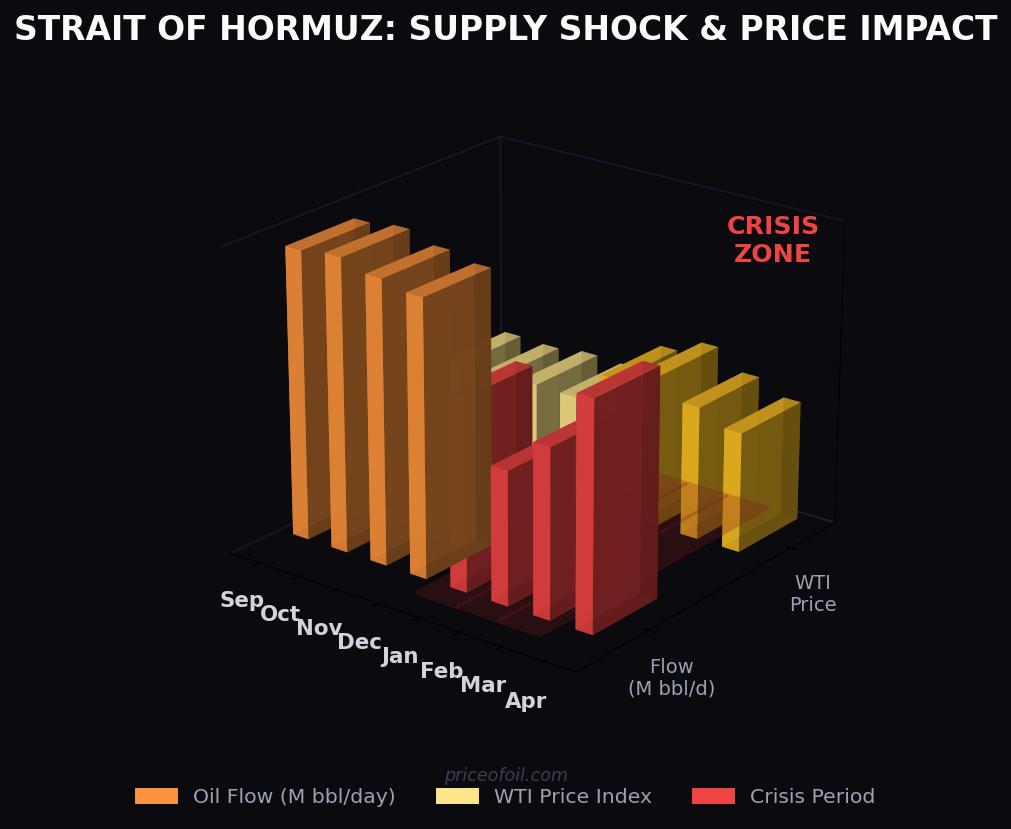

The strait has been effectively closed since March 4. Analysts at TD Securities estimate nearly 1 billion barrels of crude and refined products will be lost by month's end if the shutdown continues. That is a disruption comparable in scale to the 1970s oil shocks, compressed into a matter of weeks.

A $30-per-barrel war premium is baked into current prices. Traders are not paying $112 for oil because the world needs it at that price. They are paying it because no one knows where the next tanker gets hit.

Two Possible Tuesdays

If Iran accepts a deal before the deadline, the math is straightforward: the war premium evaporates. Analysts expect Brent to fall toward $80 within days. The global market outside Hormuz is actually well-supplied. OPEC+ has been hiking output, U.S. shale is running hard, and demand is already softening under recession pressure from the tariff cycle.

If the deadline passes without a deal, the next move belongs to Trump. He has set and extended this deadline four times. Markets are discounting some portion of that pattern. A fifth extension would confirm that the deadline is a negotiating posture, not a red line. A strike, however, would push WTI toward $130 and potentially higher depending on what infrastructure gets hit.

The problem for traders is that neither outcome trades cleanly in advance. Any leak of a deal sends prices down 5% in minutes. Any escalation headline reverses that instantly.

Gasoline Is Already a Problem

The macro debate obscures a more immediate issue: U.S. fuel prices. Regular gasoline averaged $4.19 per gallon nationwide as of Sunday, with California above $5.50. Fuel shortages have been reported in parts of the Southeast and mid-Atlantic as refinery run rates drop with heavy crude feedstocks constrained.

Every day the strait stays closed, that problem gets worse. Refiners can substitute lighter domestic crudes for some applications, but not all. The shortfall is starting to show at the pump.

What to Watch

The 8 p.m. ET Tuesday deadline is the immediate catalyst. A direct statement from Tehran or Washington before then could move prices several dollars in either direction. After the deadline, watch for any indication of U.S. military movement in the Gulf, or any counter-proposal from Iran that keeps talks alive without conceding the core demand.

The market has been living in this limbo for five weeks. It cannot stay there much longer.

This article contains forward-looking analysis based on current market conditions and publicly available information. Commodity prices are highly volatile and subject to rapid change. Nothing here constitutes investment advice.